Is Your Money Better Off In Cash Now?

Tempted by high deposit rates?

Your financial adviser will have told you how much cash to keep in the bank for day-to-day and rainy-day needs, but the best potential for your cash comes from your investment portfolio, not deposits as we shall examine in further detail throughout this article.

Deposit rates seem attractive, but they aren’t in real terms….

Current interest rates might seem like an exception, but they’re not…

Putting cash into term deposits may cost you in terms of returns more than you think, if you try to time your entry to an investment portfolio….

Cash and your portfolio

You will have worked with your financial adviser from outset to ensure that your assets are invested in a way that are most likely to meet your future financial objectives. As we will examine further, for the majority of clients this involves a portfolio of equites and bonds. Cash is put aside for short term requirements or for emergencies and you will have discussed how much is appropriate for this, bearing in mind your individual circumstances with your adviser. This provides surety of your capital, but doesn’t account for the impact of inflation, as we shall discuss.

Current interest rates and inflation

After a period of low interest rates following the global financial crisis (GFC) in 2008, we now have a level of interest rates that offer 12-month term deposits of around about 6%1. At face value, this might seem attractive. However, if one considers the current rate of inflation of 6.4%2, then that current deposit rate is negative in real terms. So, by locking up your money for 12 months or more, you are betting that inflation comes down to an extent where the return is positive. Therefore, your term deposit is not ‘risk-free’, as there is a risk that the rate of inflation may continue to reduce both the spending power of both the interest and your capital.

1 Money.co.uk 22/8/23.

2 CPI. Source: ONS 16/08/23.

Current rates are not exceptional in historical terms

There could be the temptation to think that current interest rates are an exception and therefore represent a better medium- or long-term investment given the recent returns from an investment portfolio as a result. This is not the case. If you look at information on the Bank of England website3, you will see that the average base rate for the ten years up until the beginning of the GFC (Oct 2008) was 5.11% and the twenty years up until then, 6.49%. Even if one includes the period of exceptionally low rates from 2008, the average rate for the thirty years to the end on 2022 was 4.39% and, despite these higher interest rates, equities and bonds have historically represented better value investment than cash deposits over the longer term, as we shall now examine.

3 Bank of England base rate database 23/08/23.

A reminder about why your adviser recommends an investment portfolio:

The chart below shows the respective returns of differing types of investments, including cash deposits over a 30-year period to the end of 2022:

Source: Bloomberg, Factset and Bank of England, as at 31 December 2022.

Notes: Cash = ICE LIBOR – GBP 3 month. Global Equities – The MSCI Word Index. US Equities - S&P 500. UK Equities – FTSE All Share. Inflation – Retail Price Index (Jan 1989 – 100): Global Bonds – Bloomberg Global Aggregate. European Equities – MSCI Europe, UK Gilts = ICE BofE UK Gilt (local total return), Emerging market equities – MSCI Emerging markets. All shown gross of tax and of fees and in GBP. Annualised performance refers to the entire period. Performance in the reinvestment if Income

So, even if one considers that for many years during the thirty-year period shown above, interest rates were significantly higher than the average since 2008, historically, equities and bonds offered you superior returns. The table below demonstrates those returns over an even longer time period and the impact of inflation on those returns. Although this length of data is just available for the UK market, this period included significantly higher levels of interest rates than were evident in the chart above. Of course, you should also consider any charges associated with your investment, which may have impacted those returns.

Equities and bonds do not give the capital security that cash can provide. Your capital is at risk. The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Sources: Vanguard, using Dimson-Marsh-Staunton global returns date from Morningstar, Inc (The DMS UK Equity Index, DMS UK Bond Index, DMS World Bill Index) Notes: Data covers 31 December 1900 to December 2022. Returns are in GBP. Nominal value is the return before adjustment for inflation with dividends and income reinvested, real value includes the effect of inflation. UK Treasury bills are used here as a proxy for cash.

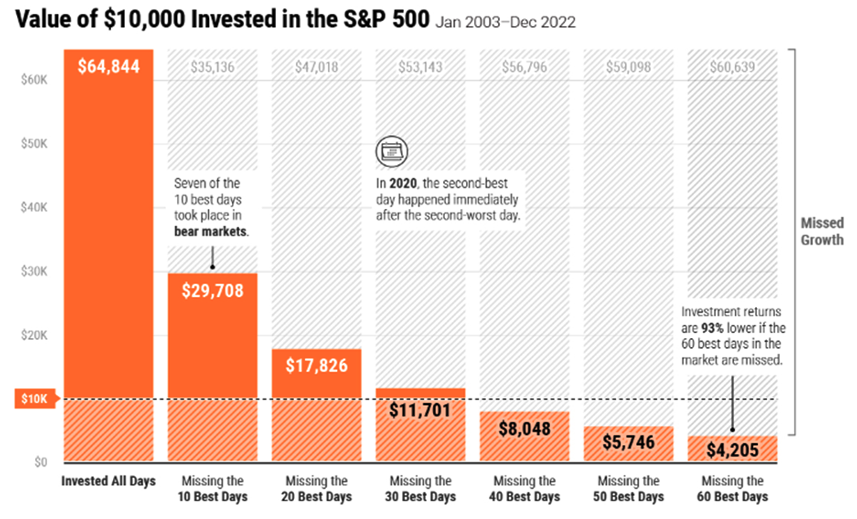

Yes, equities and bonds fluctuate in value, but that’s why you hold them for the longer term i.e., 5 to 10 years. Trying to time your investment to switch from cash to these assets is notoriously difficult and doing so brings its own risks to your potential returns. The following chart demonstrates how trying to time the market can lead to returns being compromised (we have used the U.S. S&P 500, as the U.S. market represents over 50% of the world’s stock markets by value):

Source: Marlborough, Carson Group, Visual Capitalist, Axios 16 Aug 2023

So, why do equities do so well over the longer term?

At a basic level, equity investors benefit from GPD (economic) growth, earnings growth and inflation:

GDP Growth: If an economy is growing, then companies can benefit from that growth through extra business.

Earnings Growth: Companies aim to grow their profits each year and pass these onto shareholders, either through a higher share price or dividends.

Inflation: Many companies, as we have seen recently, have simply passed on increased costs they incur through inflation onto their customers. This is then reflected in their profits.

The risk of damaging returns by holding your money in cash

We have already seen how damaging trying to time entry into the stock market can be. The following table shows the results of analysis of the possible effects of investors keeping their money in cash instead of putting it into a 60/40, equity/bond portfolio over different time frames and over a longer period of time:

Past performance is not a reliable indicator of future results.

Source: Vanguard calculations in GBP, based on data from Refinitiv

Data is based on the period between 31 January 1990 and 28 February 2022Note: The chart shows the percentage of times that cash has underperformed a global 60% equity/40% stock portfolio over 3-, 6- and 12-month periods after 2 months total returns of global equities were below 5%. For example, global equity returns from 31 August 2008 to 31 October 2008 were -20.74%. Over the following 3-month period until 31 January 2009, cash returned 0.84% while the 60/40 portfolio returned 1.76% so that the excess returns were at 0.93%. Equity comprises global equity (MSCI AC Word Total Return Index). Fixed income comprises hedged, global bonds (Bloomberg Global Aggregate Index Sterling hedged). Cash is represented by GBP 3-month deposits.

As can be seen, you run the risk of reducing your investment returns from your portfolio, the longer it is kept out of the market and in cash. Worse, term deposits usually require you to lock up your money for a fixed period, so this can exacerbate this effect.

Opportunities in bonds?

Finally, the change in the underlying interest environment, while very challenging for investors in bonds during a period of rising rates such as in 2022, does now throw up some potential opportunities for the future as we approach a likely peak interest rate. The graphs below show both the negative impact of a rising rate scenario on bonds with different expiry dates and the positive impact of a declining rate environment. Your adviser can explain why this is in more detail, but it’s because the rate of return from a bond is fixed, so as interest rates decline that fixed payment potentially becomes worth more to investors and the price of the bond will reflect that. Bonds with longer to expiry have a greater sensitivity to those changes in rates, so investment managers can choose the most appropriate expiry to suit the expected environment. So, again, tying money in term deposits, rather than leaving it to your investment manager to take advantage of any reduction in interest rates, represents a potential opportunity cost to you.

Source: Vanguard calculations, using Bloomberg data as at 31 January 2023.

Notes: The Bloomberg U.S. Treasury 1-3 Year Index had a duration of 1.86 years and a yield to maturity of 4.28%. The bloomberg U.S. Treasury 3-10 Year Index had a duration of 5.17 years and a yield to maturity of 3.62%. The Bloomberg U.S. Long Treasury Index had a duration of 16.42 years and a yield to maturity of 3.72%. Scenario assumed any interest changes occur at the beginning of the period and before any reinvestment of dividends. Scenario does not convexity into account, This illustration is hypothetical and does not represent the return on any partciular investment and the rate is not guaranteed.

Conclusion

While the change to the interest environment since 2021 may seem to make cash deposits more attractive, we should remember the impact of inflation on these returns. If rates go down longer term, so will your returns from your cash on deposit. Likewise, these now higher rates should not distract us from the longer-term benefits of an equity/bond portfolio, which offer far superior returns over the medium to long term.

IMPORTANT INFORMATION

This document is written in conjunction with Rockhold Asset Management Ltd and its content is for your general information purposes only and does not constitute investment advice. The commentary is intended to provide you with a general overview of the economic and investment landscape. It is not an offer to purchase or sell any particular asset and it does not contain all of the information which an investor may require in order to make an investment decision. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of this article.

Farrmore Limited is an appointed representative of Sense Network which is authorised and regulated by the Financial Conduct Authority Registered in England and Wales, 4952745. Registered office: 1-3 Dunham Road, Altrincham, WA14 4NX