Investment Update - August 2023

Overview

July was another buoyant month for global stock markets, which were mainly in positive territory. The broad US market, as represented by the S&P 500, is now up over 20% in local currency terms year to date (although, for sterling-based investors, this return was dampened by around 6% due to a resurgence in the pound). The standout market was China, with locally traded A shares up around 6% in sterling terms. This followed announcements by communist party officials there that they would be taking steps to stimulate the economy (albeit short in detail of what these steps might be).

The UK market also experienced a recovery. What is of particularly interest is to see how the market rallies broadened out. It has been reported here on a number of occasions about the narrowness of the rally in the US, with the S&P 500 being driven by only 7 ‘mega’ stocks.

However, in July we saw both wider contribution within the main index as well as mid and small cap indices outperform, both in the US and globally, perhaps representing confidence in the prospects for the wider market than previously. The bond markets, however, continue to conflict with that narrative, as yields continue to climb and in a way that usually signifies economic slowdown or recession. Given the extended valuations of stocks, particularly in the US, this would suggest that they are vulnerable to any disappointment on the corporate earnings front.

US

Much of the optimism in the US stock market was led both by a perception that US interest rates have peaked coupled with a positive earnings backdrop, with around 80% of companies reporting earnings that exceeded analysts’ estimates. Whilst we saw another quarter point rise in interest rates to a range of 5.25 -5.5%, its highest level for 22 years, markets seem convinced that the raising cycle is over now. This was despite US Federal Reserve Chairman, Jerome Powell, stating that he would not hesitate to raise rates again if inflationary pressures resume. However, for now, inflation continues to wane. Recession certainly did not arrive in the US in Q2, with GDP coming in at a better-than-expected rate of 2.4% annualised. What surprised markets most was the ramp up in capital expenditure and investment in infrastructure, with a possible reshoring narrative starting to take hold. The US job market remains strong and employers are perhaps “hoarding labour” in the expectation a slowdown will be short and shallow. Employers have discovered, post pandemic, that hiring and retaining quality staff is anything but easy – they will therefore endeavour to hang on to the best hires for as long as possible. Given the current market mood, it is likely that the market will continue to move ahead. However, we cognisant of the fact that some of the impact of higher rates may not be felt until later, due to the longer term (e.g., 30 year plus fixed rate) nature of the mortgage market, therefore insulating many homeowners from rate rises. In addition, companies when they refinance will be doing so at significantly higher rates than before.

Accumulated personal savings from the “helicopter money” President Biden handouts are waning. US mortgage costs are much higher for those new borrowers and those refinancing. It is therefore likely that the impact of higher rates won’t be reflected until later in the year or early into 2024.

UK

In the UK, much of the focus has been on the more persistent nature of inflation and, as elsewhere, speculation over the future direction of interest rates. Such was the extent of the pessimism that at one point during early July, the 10-year gilt yield exceeded the peak of the spike in UK bond yields following 2022’s Kwarteng budget debacle. The shorter time horizon, 2-year bond yield, at one point exceeded 5.5%. However, a better than expected inflation rate print of 7.9% for June contributed to bond yields falling steeply later in the month and this was accompanied by a corresponding 400 point rally in the FTSE 100. As previously reported, this rally extended to the wider mid and small cap indices. The UK stock market is, from a historical perspective, cheap from a valuation perspective, but it does face headwinds form a more uncertain economic backdrop and its over reliance on resource related stocks.

Europe

Europe, as elsewhere saw steady returns across the continent and likewise a broadening of the rally into mid and small caps. July saw the ninth consecutive interest rate rise for the European Central Bank (ECB); a 0.25% increase brought the deposit rate to 3.75%. Christine Lagarde has said ‘There is a possibility of a hike, there is the possibility of a pause’ in September and policy makers are ‘open minded’. Following this, the July core inflation numbers released were slightly disappointing as they remained at the same level as June, 5.5%. That said, inflation has almost halved since October 2022, this is in part due to a decline in Energy prices.

Japan

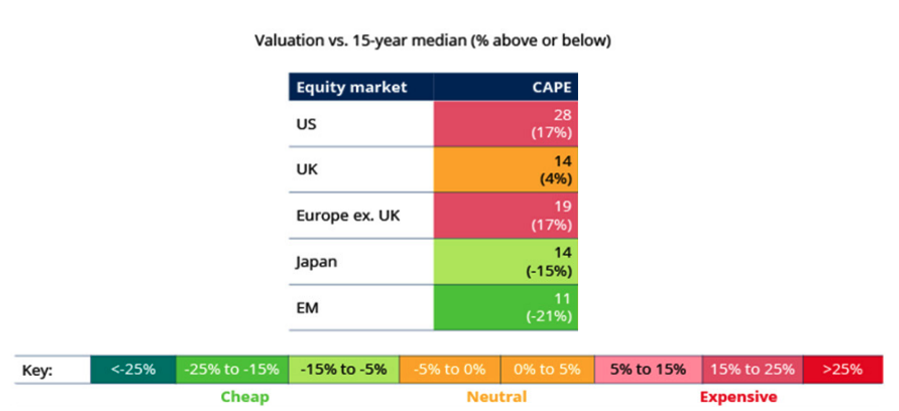

Although the stock market paused for breath in July, the market is still attracting overseas attention following the relaxation of the Bank of Japan’s yield curve control policy, which previously capped the yield on Japanese bonds at 0.5% and now tolerates a level of 1%. This makes Japanese bonds more attractive to domestic investors and markets perceive that this would lead to a continuation in the recent trend of repatriation of overseas assets held by Japanese institutions. Interest rates still remain low in Japan, relative to the rest of the world and this could stimulate economic growth. Despite the rally since the start of the year (over a 11% in sterling terms), the market is still considered cheap, especially when compared to overseas markets and the market’s historical average valuation. The chart below demonstrates this by looking at the CAPE ratio, which is a cyclically adjusted representation of a market’s price compared to the earnings generated by the constituent companies. A negative figure suggests a market is below its 15-year median (EM = emerging markets).

Sources: Datastream Refinitiv, MSCI and Schroders Strategic Research Unit. Data to 31 May 2023. Figures are shown on a rounded basis. Assessment of cheap/expensive is relative to 15-year median.

Asia and Emerging Markets

It was a strong month for both Asian and Latin American markets alike. Asian market performance was driven by China, where its leaders flagged support for the ailing economy, which is being affected by deflationary pressures, lack of domestic demand and a highly indebted property sector. There wasn’t much in the way of detail, but the wording used, as often is the case with Chinese politicians, contained sufficient coded statements as to suggest these areas would be addressed by policy. It is likely that some detail will be provided at the 20th party congress in the autumn.

Outlook

Positions have been increased in short-dated bonds in the UK, as these will be the immediate beneficiary of a peak in rates here once it emerges. Similarly, exposure to overseas bonds with a greater duration (sensitivity to interest rates) has been increased due to greater clarity over rates and this action is likely to continue in the near future. Bonds tend to be a beneficiary to slowdowns in economies and inflation, as central banks start to ease policy after a particularly aggressive rate hiking cycle. The combination of higher yielding cash funds, combined with higher European, Japan and China weightings is providing a good combination of balancing risk with returns. We may well see a reduction in US equities short term, as the rally continues to develop, once our investment processes signal that this might be prudent.

With contribution from Rockhold Asset Management, Alpha Beta Partners, LGT and Marlborough, August 2023

Your Capital is at risk. Past performance is not a reliable indicator of future results. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. Your capital is at risk and the value of investments, as well as the income from them, can go down as well as up and you may not recover the amount of your original investment.

IMPORTANT INFORMATION

This document is written by Rockhold Asset Management Ltd and its content is for your general information purposes only and does not constitute investment advice. The commentary is intended to provide you with a general overview of the economic and investment landscape. It is not an offer to purchase or sell any particular asset and it does not contain all of the information which an investor may require in order to make an investment decision. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of this article.

Farrmore Limited is an appointed representative of Sense Network which is authorised and regulated by the Financial Conduct Authority Registered in England and Wales, 7563763. Registered office: 1 Dunham Road, Altrincham, WA14 4NX