Market Update - April 2023

Market Update - April 23

Financial headlines in March were dominated by the failure of Silicon Valley Bank (SVB) and the apparently arm-wrestled merger of Credit Suisse with UBS by Swiss regulators. Unsurprisingly, equity markets reacted negatively to the news about SVB and initially took a tumble, which was naturally led by banking sector stocks. However, once investors had stepped back and begun to analyse the situation and aided by the US Federal Reserve’s (the Fed) reassurance that all banking deposits were insured by them, some calm returned to the market. It is worth observing that SVB, as a bank capitalised at under $250bn, was subject to less regulatory controls than those covering larger banks in the US, or that exist for banks generally in Europe. Therefore, while some concerns still exist over some smaller banks in the US, the current situation is not seen by most as a repeat of the banking crises in 2008.

Whilst we look at the drivers behind it later, what was encouraging to the normally diversified investor was the way that fixed interest stocks (bonds) behaved during this particular sell-off in equities. Since late 2021, we have seen bonds correlate highly (i.e. move in the same direction) with equities, which is abnormal. However, on this occasion they moved in the opposite direction (as demonstrated by the chart of the FTSE All Share and UK Gilts’ price movements in March below) and thus resumed their place as a diversifier during periods of uncertainty.

Source: Morningstar

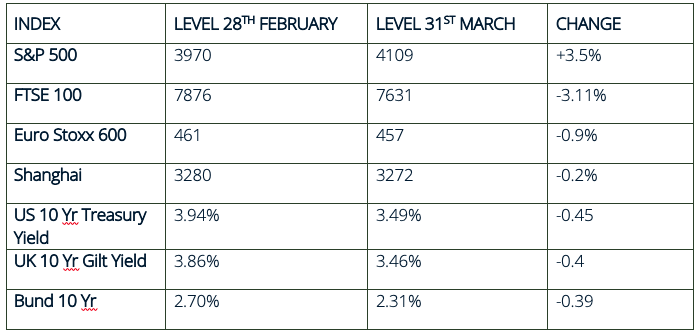

US

In the US, while stocks initially fell on news of SVB’s demise, once the Fed had provided the necessary reassurances about the banking sector, equity markets then began speculating that the impact of the event might impact lending, and thus hasten the end of the interest rate tightening cycle by the Fed. This in turn led to significant rally in interest rate sensitive stocks, such as technology companies. Consequently, we saw the US broader market finish up 3.5% over the month and the technology company rich Nasdaq index, up over 6%. Bonds were also up over the month, due to the same speculation about interest rates. Neither market was perturbed by the fact that the Fed continued to increase interest rates post-SVB to 4.75%. Central bankers will no doubt be monitoring the effect of SVB on credit markets to determine if there is any impact on the economy and inflation over the coming months. Meanwhile, we will soon move into earnings reporting season in the US, which should give investors some idea as to whether the significant tightening cycle by the Fed is having an effect on corporate earnings, with the market seemingly suggesting a decline of around 6%. However, we have seen companies using the inflationary backdrop to increase margins. So, given the still quite high valuations, this could prove a test for markets.

UK

The impact of SVB on the UK equity market was more pronounced, due to the high exposure to the banking sector in the major indices. There was also a sharp drop in the oil price, which fell $10 around the same time. This exacerbated the market falls, given the dominance of the oil majors in the index. Towards the end of the month, OPEC announced a cut in production, which boosted the oil price and energy companies’ share prices, but the UK market was still one of the worst performers during the month. Inflation figures released during the month surprised to the upside with February CPI rising to 10.4%, compared to 10.1% in January. The drivers of the increase were mainly food prices which increased 18% over the year. In contrast, other constituents of the CPI basket are seeing annual increases moderate, such as transport and motor fuel which only increased 2.9% and 8.7% respectively. As we move through the year, the base effects of the higher energy prices last year and the significant falls we have witnessed are expected to drive the annual inflation figure lower.

Europe

Headline inflation data for the Euro area came in lower than expected for March. The reading of 6.9% compared with 8.5% a month earlier and consensus forecasts of 7.1%. This is the region’s lowest level in a year. That said, it was not all good news, with core inflation rising to a new record high of 5.7%, well ahead of central bank targets of 2%, which continues to put pressure on officials to continue with rate rises. Although there are concerns of a credit crunch caused by banking sector turmoil, the area also has strong wage inflation and employment numbers to consider.

Japan

March saw the final policy meeting for Governor Kuroda before retirement and as expected there were no changes in monetary policy. Core Inflation reached its lowest level in five months - data from February showed a rise of 3.1%, which was a sharp fall from the 41-year high level of 4.2% in January. This is thought to be a result of energy subsidies feeding into the data, following an economic stimulus package announced last year which saw a 20% discount on household electricity prices. Looking ahead, April will see the Bank of Japan’s first leadership change in a decade as Kazuo Ueda takes the helm as Governor.

Asia and Emerging Markets

March saw inflation continuing to fall across Asia and Emerging Markets, and it is typically at levels much lower than the UK and Europe. In contrast, geopolitical tensions remain heightened, be it US-China or China-Taiwan. Chinese officials visited both Russia and Ukraine in an attempt to broker a ceasefire, which other countries branded as biased towards Russia. During the month, some industrial and manufacturing data was not as strong as expected. It highlighted that China’s reopening has not provided the broad boost to every sector and is more targeted. That said, there is still a boost, and it is expected to benefit the wider region, not just China.

With contribution from Alpha Beta Partners and Marlborough, April 2023

IMPORTANT INFORMATION

This document is written with Rockhold Asset Management Ltd and its content is for your general information purposes only and does not constitute investment advice. The commentary is intended to provide you with a general overview of the economic and investment landscape. It is not an offer to purchase or sell any particular asset and it does not contain all of the information which an investor may require in order to make an investment decision. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of this article.

Past performance is not a reliable indicator of future results. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. Your capital is at risk and the value of investments, as well as the income from them, can go down as well as up and you may not recover the amount of your original investment.

Farrmore Limited is an appointed representative of Sense Network which is authorised and regulated by the Financial Conduct Authority.

Registered in England and Wales, 7563763.

Registered office: 1 Dunham Road, Altrincham, WA14 4NX