A New World For Investments

2020 - 2023

A NEW WORLD FOR INVESTORS

Investment Nirvana

The world as we entered 2020 had been a pretty benign environment for investors for decades. Yes, we had hiccups along the way for equity investors, such as Black Monday, the Tech Bubble, the Global Financial Crisis to name a few, but markets recovered and, crucially, diverse portfolios, which included lower risk bonds helped dampened the falls accompanying these events. They were all assisted by the backdrop of ever declining bond yields and interest rates, as the chart below demonstrates:

This environment was helped by disinflation, partly caused by increased globalisation of commerce and the sourcing of lower costs for businesses by steadily moving production and services overseas (remember ‘Made in Hong Kong’ labels on products?). Indeed, even up to 2021, banks were concerned about deflation, which was supportive for rates going lower. The lower cost of money coupled with a lower inflation environment was supportive for businesses, and thus share prices, whose valuations gradually expanded. The chart below shows how Price/Earnings ratios (a measure of valuation) went up from 1980 onwards.

It was also incredibly supportive for bond prices, as demonstrated by the performance of UK medium dated gilts in the years preceding 2022:

Indeed, by the time we got to the 2020’s, many, now highly qualified market participants had no experience of any alternative environment and many investment processes were shaped by only ten or twenty years of historic data, which was absolutely fine…..until everything changed in 2020.

The Great Diaspora

We will not dwell on the causes of the shift to a high inflation environment that occurred at the end of 2021, but COVID was a major contributor and most significantly Central Banks’ reaction to it that set the wheels in motion. Unfortunately, so convinced were central banks about their success in controlling inflation since the eighties, they failed to notice the impact of their policies on demand, whilst supply lines were continually compromised. Indeed, even as we all saw inflation picking up significantly towards the end of 2021, central bankers were still concerned about deflation, infamously describing inflation as ‘transitionary’. We all know now that they were wrong.

The impact of a generational shift in the inflationary environment was extremely significant. In 2020/21 plenty of cheap money was circulating, courtesy of central banks. Symptomatic of this was the fact that investors were even prepared to invest billions in ‘Special Purpose Acquisition Companies’ (SPACs). These were essentially start up vehicles with no operational structure but had a loose business plan to acquire businesses and merge them. They relied on cheap money to fund themselves. However, equity valuations are sensitive to interest rates, as are bonds (which we shall come on to). So, the Federal Reserve’s volte face when they suddenly realised that they were catastrophically wrong about inflation being ‘transitory’, led them to push up interest rates up rapidly, which in turn caused what had become excess equity valuations to react i.e. share prices fell. Growth companies, particularly technology ones, were hardest hit, as their valuations were the most sensitive to interest rates going up. Meta, the owner of Facebook, saw it’s share price decline by over 70 percent at one point. This was reflected in the tech heavy NASDAQ index in the US, which fell by 34 percent. Other stock markets globally followed this, albeit to a lesser extent. This represented the end of the cheap money speculative bubble and many of the aforementioned SPACs have gone on to struggle or fail as a result.

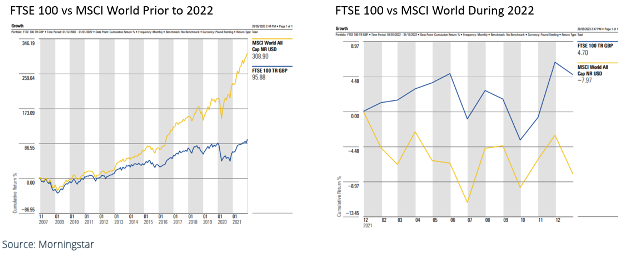

For normally diversified investors, the effect of this new environment was unprecedented. Bond prices are based on current interest rate levels, so when we saw rates quadruple, this had an extremely negative effect. So, the ‘haven’ asset not only didn’t dampen the falls in equity markets, in many cases they were as bad as, if not worse than, equities. The chart below shows different global bond indices during 2022:

In contrast to the US, the UK market’s FTSE 100 index, which had previously been a dampener on portfolios, due to its disproportionate exposure to energy, commodity, banking and consumer durable stocks, suddenly found itself the only major equity market to go up in 2022. This was as energy and commodity prices surged and, to its advantage, the FTSE was also regarded as a cheap ‘value’ market.

The past is the past, what about the future outlook?

Events over the last three years have conspired to lead to disappointing results for investors (unless you only owned the FTSE 100 index, which we shall come on to). So, what are the prospects now? Well, firstly, it should be remembered that markets are always looking forward, so they tend to start to price in future events generally earlier than the general populus experience them.

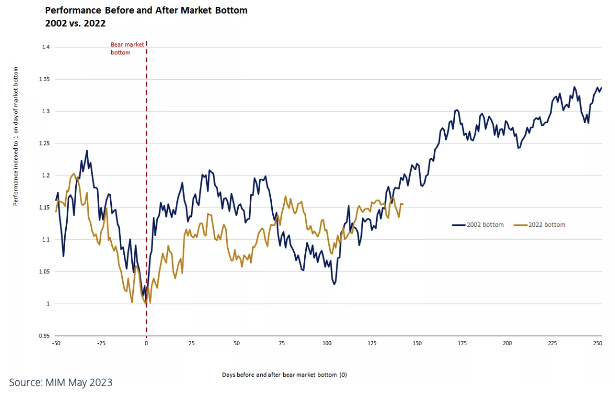

Looking at the economic backdrop, it is evident that the tighter monetary policy environment that the US Federal Reserve has created does seem to have led to peak inflation and even in the UK, which has its own set of unique problems, the rate is declining. This suggests that, starting with the US, we are likely to see peak interest rates soon i.e. a pause in increasing interest rates (the UK is some way behind). What is currently unclear is how long they will stay at those peaks, when they will start to decline, the impact on the economy in the interim and thus corporate earnings. Markets hate uncertainty and it is likely we will some continued volatility in equity prices between now and Q4 2023, when we will probably have a clearer idea as to the future direction of rates. The chart below perhaps provides some idea as to where we might be in the cycle. It illustrates the performance of the S&P 500 50 days before, and 250 days after, the 2002 & 2022 market bottoms. So far, the performance of the index since the 2022 bottom has been comparable to the market performance following the 2002 bottom. A mild recession this year remains possible, but it may not look or feel like prior recessions due to a better-positioned consumer. As a result, it is likely that the stock market's lows last October captured a good portion of this outcome, meaning that even if a recession emerges this year, it does not have to be accompanied by a drop to new lows for equities, but it is possible.

So, while this is reassuring given the US is the world’s largest stock market, what about the UK? Well, the FTSE 100 is peculiar in its makeup, as described earlier. As such, it cannot really be described as a market for growth companies. We have seen recently that some growth companies, such as ARM holdings, have chosen to list their shares in the US rather than the UK. Worse, many of the international companies currently listed in the UK are vulnerable to switching their listing to the US, as they eye a more liquid market for their shares and a possible share price premium. Some of those factors such as higher energy prices and the allure of value stocks which buoyed the FTSE 100, are now dissipating. So, while there may be some attractively priced growth companies in the UK market, it is not the broad market that is likely to benefit long term. However, as we are global investors and the UK is only 4% of the world’s stock markets, this is not a major concern for us.

Turning to bonds, which have since November 2021 been a drag on portfolios, what is the outlook there? Well, the answer is probably quite positive too. If one follows the logic that if increasing interest rates and inflation are bad for bond investments, then the reverse is also true, so a declining inflation and interest rate environment should be positive for bonds. In addition to this, bond yields that investors are able to lock into now are much more attractive than in 2021. The forward-looking returns in the UK back then were in the region of 1%, which reflected the environment of low inflation and rates at the time. Now, the forward-looking annual returns are more in the region of 5% (source: Vanguard Jan 23). Couple this with declining interest rates and prospects looking forward seem positive. As investors, we just have to be careful about timing our entry points this year.

A final reminder

Equity bear markets are normal, and we expect them to happen, however, they are less frequent than bull markets and, as the chart below demonstrates, have less of a negative impact than bull markets have a positive, on long term returns:

The important take away, is that you need to stay invested through bear markets in order to benefit from the long-term gains from bull markets, as attempting to time market cycles is notoriously difficult.

Past performance is not a reliable indicator of future results. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. Your capital is at risk and the value of investments, as well as the income from them, can go down as well as up and you may not recover the amount of your original investment.

IMPORTANT INFORMATION

This document and its content is for your general information purposes only and does not constitute investment advice. The commentary is intended to provide you with a general overview of the economic and investment landscape. It is not an offer to purchase or sell any particular asset and it does not contain all of the information which an investor may require in order to make an investment decision. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of this article.

Farrmore Limited is an appointed representative of Sense Network which is authorised and regulated by the Financial Conduct Authority Registered in England and Wales, 7563763. Registered office: 1-3 Dunham Road, Altrincham, WA14 4NX